Option Workshop, version 18.2.1657

Polynomial volatility model, notifications through Telegram and Market-maker ergonomic improvements

Polynomial volatility model, notifications through Telegram and Market-maker ergonomic improvements

In this update, we’ve added several improvements: copying a strategy with all fills, a new Mnns (moneyness) column that shows the option status, the ability to bind the Charts form with the active (selected) strategy in the Positions manager, the ability to display the P&L chart taking the commission for the fills into account, etc.

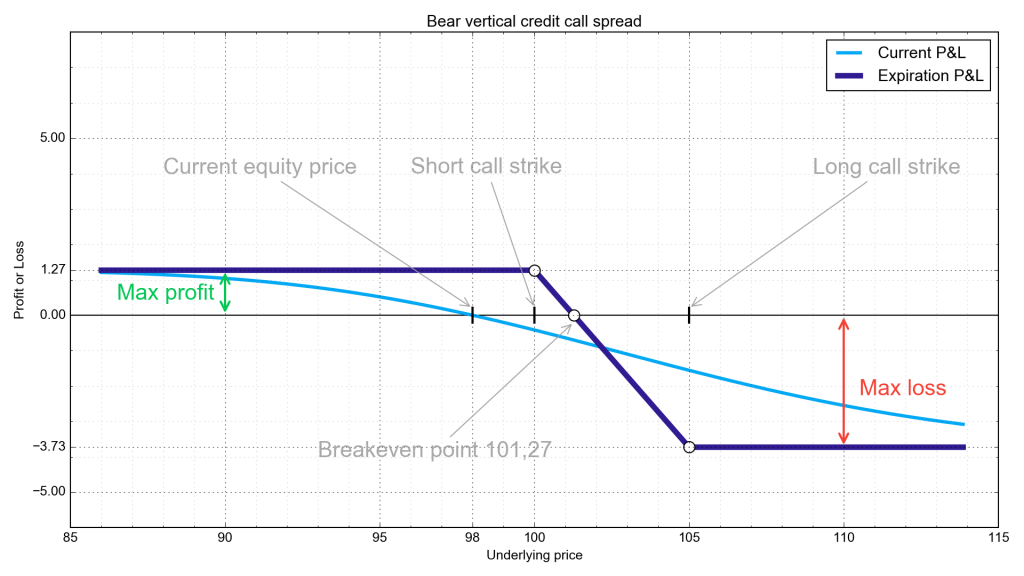

Bear Call Spread. An alternative name is Credit Call Spread. Bearish position. It is a vertical spread involving an equal number of long and short calls on the same underlying asset and with the same expiration date. It is a credit spread, which means you receive money to put on the position. The strategy profits as long as the price of the underlying security remains below the breakeven point.

We've released a small update, which includes only two bug-fixes: The program sometimes hangs when user try to change position price through the Set price button; The program ignores the first line of a CSV file with volatility curve.

In our new version, we have changed the principle of pricing models setting. Now the model is defined as a pair of a computation model (Black, Black-Scholes or Cox-Ross-Rubinstein) and volatility model. You can create multiple models for each series of options and customize them in different ways.

The main change of the new version is an ability to customize the line styles for the volatility skew: model lines and markers. Also we continue to improve the functionality of Option Workshop and fix some bugs.

Today we’re going to talk about how we calculate volatility in Option Workshop, and what our plans are to improve this part of the functionality. Option Workshop is integrated with several data sources, which provides market data for options and their underlyings.